2025 was a positive year for the quantum technology industry, marked by continued technical progress contributing to market growth, and increases in public and private investment, pure-play quantum companies, and workforce. The United Nations’ designation of 2025 as the International Year of Quantum Science and Technology and the 2025 Nobel Prize in Physics being awarded for quantum physics experiments helped elevate the industry by promoting international collaboration and encouraging policymakers and institutions to highlight quantum technologies in their innovation agendas. This report reflects the global quantum technology industry as of the end of 2025, and underscores that the industry is maturing and gaining strategic importance worldwide.

Jump to:

QED-C seeks to capture key metrics that characterize the size and impact of the global quantum industry in a way that can be tracked and compared over time.

Inspired by Harvard Business School’s Balanced Scorecard, QED-C applied a similar analytical framework to the quantum industry. This State of the Global Quantum Industry 2026 report provides a data-driven perspective on the industry composition, investment, market size, workforce, and intellectual property. The data on which the report is based are current as of the end of 2025, with historical and forward-looking comparisons made where possible. This methodology describes the sources of data used in the April 2026 report, how these sources were used, and the limitations of the data and analyses presented. It is fundamentally the same as the methodology employed for the prior report, with additions and refinements incorporated as applicable.

The Methodolgy chapter can be found inside the main State of the Global Quantum Industry Report. Use the form above or click the button below to download.

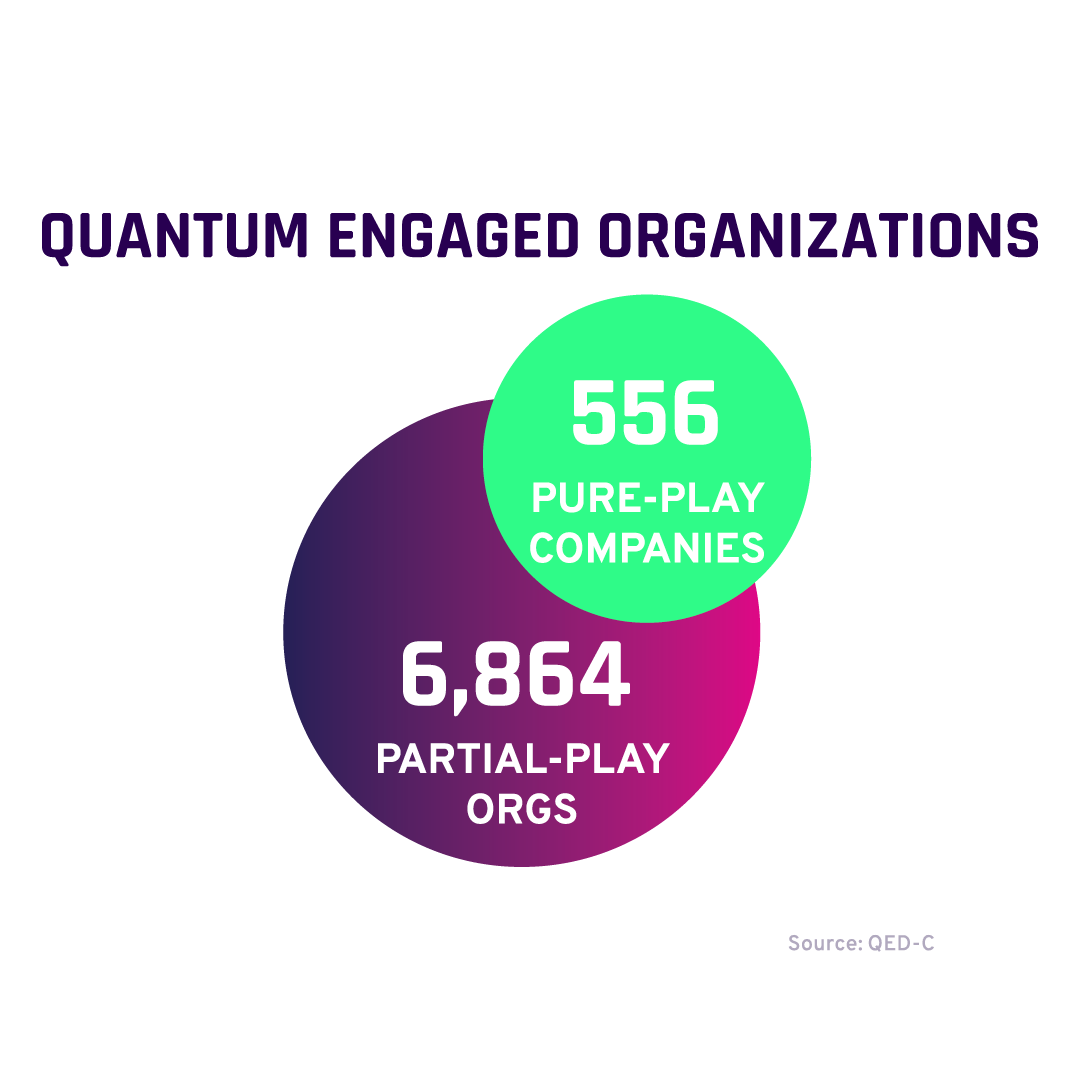

7,420

Quantum Engaged Organizations

+14% since 2024

556

Pure Play Quantum Companies

+8% since 2024

$1.9B

2025 Market Size

30% Average Annual Growth

$12.7B

NEW Government Funding Commitment

in 2025

+310% versus 2024

$4.9B

New Private Venture Capital in 2025

+192% versus 2024

16,482

Pure-Play Workers Advancing QUantum

+14% Since 2024

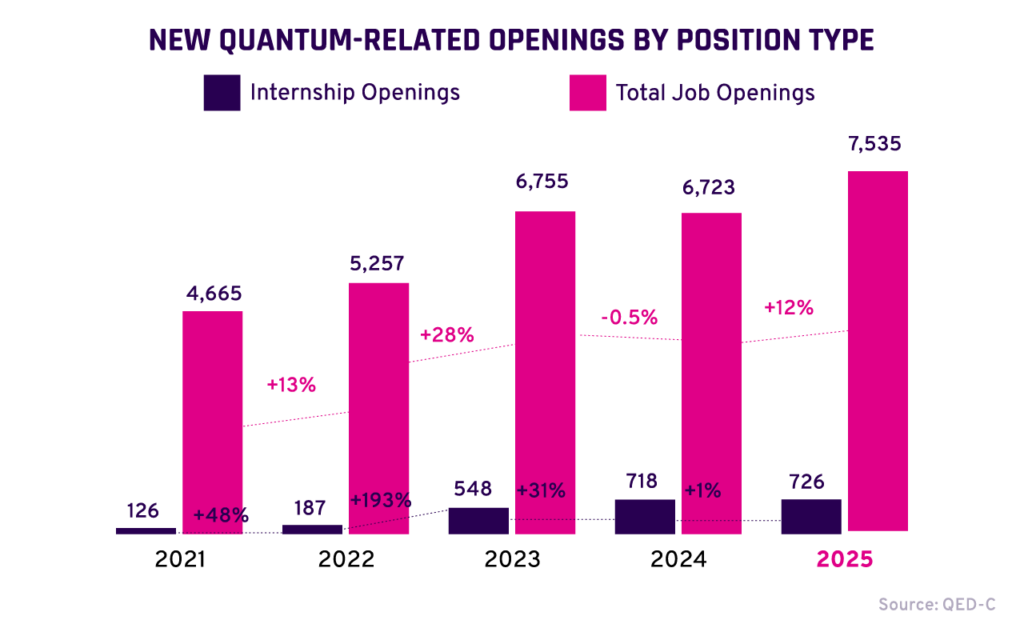

8,261

New QUantum-Related Position Openings in 2025

+11% versus 2024

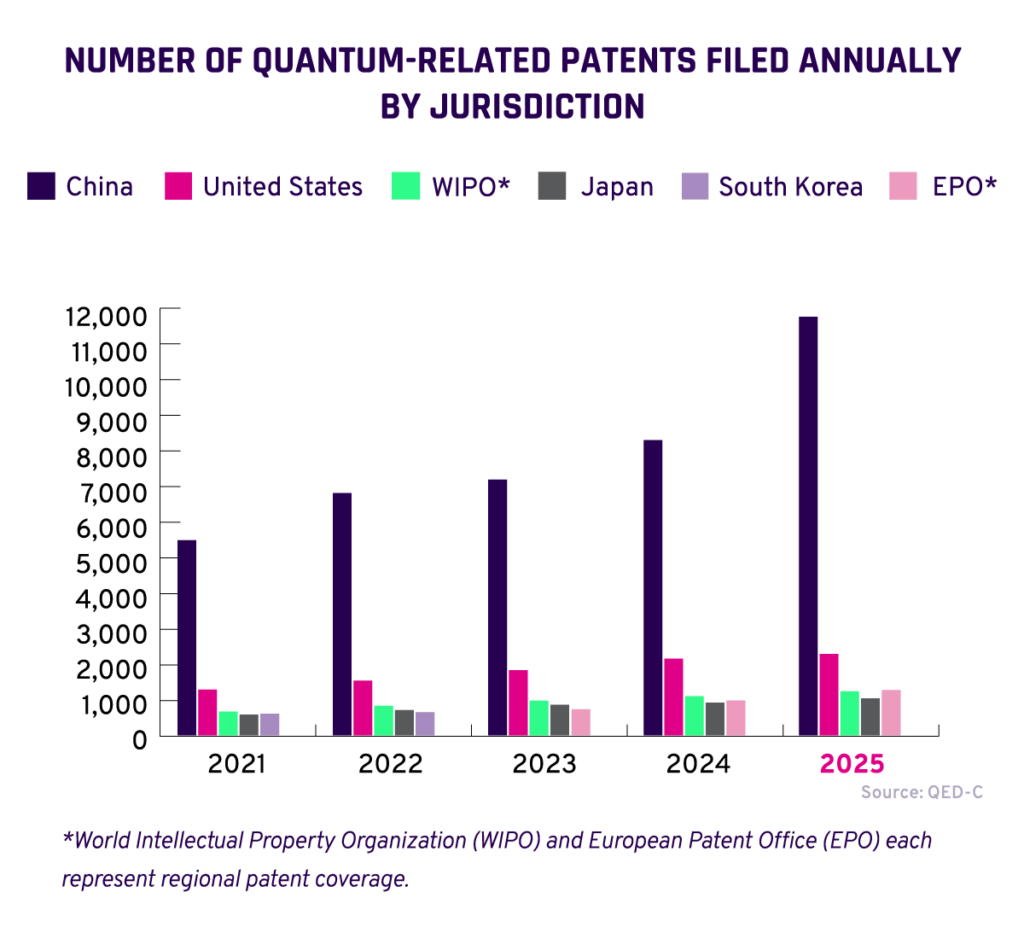

69,807

Active Patents

20% Average Annual PAtent Growth over Late Five Years

As the Quantum industry continues to scale, enterprise leaders, investors and policy makers are asking about workforce development, use cases, public private partnerships and supply chain. Here are some of the most common questions we get:

Short answer: Not yet—and that’s one of the biggest constraints on scaling.

Qualified quantum talent is in short supply and the growth in jobs in industry, universities, and national labs is creating increased demand. The quantum workforce is made up of specialists with a variety of skills and expertise, ranging from physics and electrical engineering to photonics and computer science. There is a particular shortage of talent that can bridge disciplines—e.g., quantum physics + engineering, or quantum + software development. While university programs and national initiatives are expanding the pipeline, near-term growth will depend on upskilling existing talent (AI, HPC, semiconductor engineers) and building more applied training pathways. For enterprises, this means workforce strategy—not just technology strategy—should be a priority today.

Short answer: It’s custom, fragile, and increasingly strategic.

Unlike more established tech sectors, the quantum supply chain is still developing, with critical dependencies on specialized components such as cryogenics, control electronics, photonics, and rare materials. Many suppliers serve both research and commercial markets, limiting scalability. Systems are rapidly evolving and have stringent requirements that are not yet standardized. Governments are starting to view parts of the quantum supply chain as strategically important, similar to semiconductors. Expect increased public and private investment and efforts by governments to strengthen supply chains in their region over the next 3–5 years.

Short answer: They are essential—and currently driving much of the progress.

Quantum technologies are still too early-stage and capital-intensive for the private sector to advance alone. Public-private partnerships (PPPs) help create linkages among the various stakeholders to de-risk the technologies, support costly infrastructure, and align national priorities with industry needs. Leading regions (U.S., EU, UK, Japan) are investing heavily through coordinated programs that bring together government, academia, startups, and large enterprises. The effectiveness of these partnerships will increasingly determine regional competitiveness and commercialization timelines.

Short answer: Early applications will be in simulation of new materials for medicine, energy, and space. The first useful applications are expected in 3 to 5 years.

While fault-tolerant quantum computing is still years away, near-term applications are developing in areas such as materials science (e.g., battery chemistry) and drug discovery. Other applications include complex optimization for applications in logistics and finance. Demonstrations are showing advantage in niche areas and are critical for building enterprise understanding and readiness. Organizations that start experimenting now will be better positioned to capture value as hardware improves.

Short answer: Progress will be gradual, but early positioning matters.

Quantum is not a “wait-and-see” market—it’s a “prepare-and-shape” market. Quantum computing is fundamentally different from classical computing and therefore will create new approaches to doing business. For enterprises, the risk is not investing too early—it’s falling behind in building internal understanding and strategic positioning. Opportunites for innvestors range from longer term, including fault-tolerant quantum computers, to nearer term quantum sensors, to the “picks and shovels” that are critical components.

Quantum technologies are entering a new phase—shifting from research-led exploration to early commercial traction. Quantum sensing is advancing toward broader adoption, projected to grow from ~$470M in 2025 to $1.1B by 2028, while quantum computing is scaling rapidly from a $1.4B market to more than $3B over the same period. Across both segments, growth is accelerating, use cases are expanding, and the market is taking shape in real terms.

QED-C members can access the full market forecasts below for a deeper look at where—and how fast—this industry is moving

The State of the Global Quantum Industry 2026 report offers regional overviews of quantum ecosystem development and examines major regional and global trends and key activities shaping the quantum industry. Areas of particular analytical interest for the regional assessments include pure-play companies, workforce, and investment, as well as highlights related to enabling policies, partnerships, and infrastructure. Overall, the global quantum industry is growing in terms of workforce, investment, and technical capabilities, signaling the industry’s continued economic progress.

QED-C members can access the Regional Analysis and Global Trends below.